The Seizure: What Happens When the Ceasefire Runs Out

The US seized an Iranian cargo ship in the Strait of Hormuz Sunday. The ceasefire expires Wednesday. Iran says talks may not happen. This is the update that changes the probability distribution on energy markets and AI capital economics.

The United States Navy seized an Iranian cargo ship in the Strait of Hormuz on Sunday. Iran's Revolutionary Guard has warned of retaliation. Peace talks in Pakistan may not happen. The ceasefire expires Wednesday night, and President Trump has said extending it is "highly unlikely."

This is not a ceasefire development. This is the beginning of the end of the ceasefire.

The economic implications of that distinction are substantial — and largely absent from the coverage that has treated this as a diplomatic update rather than a market event.

What happened

On Sunday, the guided-missile destroyer USS Spruance (DDG 111) disabled the propulsion of the Iranian-flagged cargo ship Touska in the Strait of Hormuz. U.S. Central Command released video of Marines descending by rope to board the vessel. President Trump said the ship "failed to heed repeated warnings" and that the military "blew a hole in the engine room" before taking control.

Iran's Revolutionary Guard responded with a warning that it "will take action against the U.S. military for the seizure," according to Iranian state media (IRNA). Iran's Foreign Ministry said Tehran has "no plans yet" regarding a second round of peace talks, accusing the U.S. of lacking "seriousness in pursuing a diplomatic process."

A U.S. delegation led by Vice President Vance, along with envoy Steve Witkoff and Jared Kushner, has headed to Islamabad anyway, where preparations were underway Monday despite questions about whether Iran would attend. Pakistan has given no formal indication of its ongoing mediation status.

The first round of talks, held roughly ten days ago, concluded without agreement. Vance accused Iran of being unwilling to accept U.S. terms on nuclear enrichment.

The economic picture before Sunday

This publication has been tracking the compound crisis affecting the AI capital buildout since early April. The logic is not complicated: the $600 billion-plus AI infrastructure commitment made by major tech companies between 2024 and 2026 was modeled on three assumptions — cheap energy, cheap money, and stable supply chains. All three are now under pressure simultaneously.

The $126 Barrel Problem documented the original energy shock. The Ceasefire Asterisk noted that even a ceasefire would leave energy market scarring. The Jet Fuel Squeeze covered the aviation specific shortage. The Convergence Point closed the cheap-money thesis when March CPI hit 3.3%.

The Independence Premium, published yesterday, addressed the third dimension: what happens to the cost of long-duration capital when the institution that prices it — the Federal Reserve — faces questions about its independence at the same moment Kevin Warsh faces a confirmation hearing.

Sunday's seizure is the update to all of these.

What has changed

Before Sunday, the situation was: ceasefire technically in effect, U.S. naval blockade continuing, Strait partially accessible, diplomatic process underway. Energy markets were pricing a prolonged but manageable disruption — elevated costs, but with a visible path to resolution.

After Sunday, the situation is: a kinetic act in the Strait itself, Iran threatening military response, talks in doubt, ceasefire expiry 48 hours away with no extension expected.

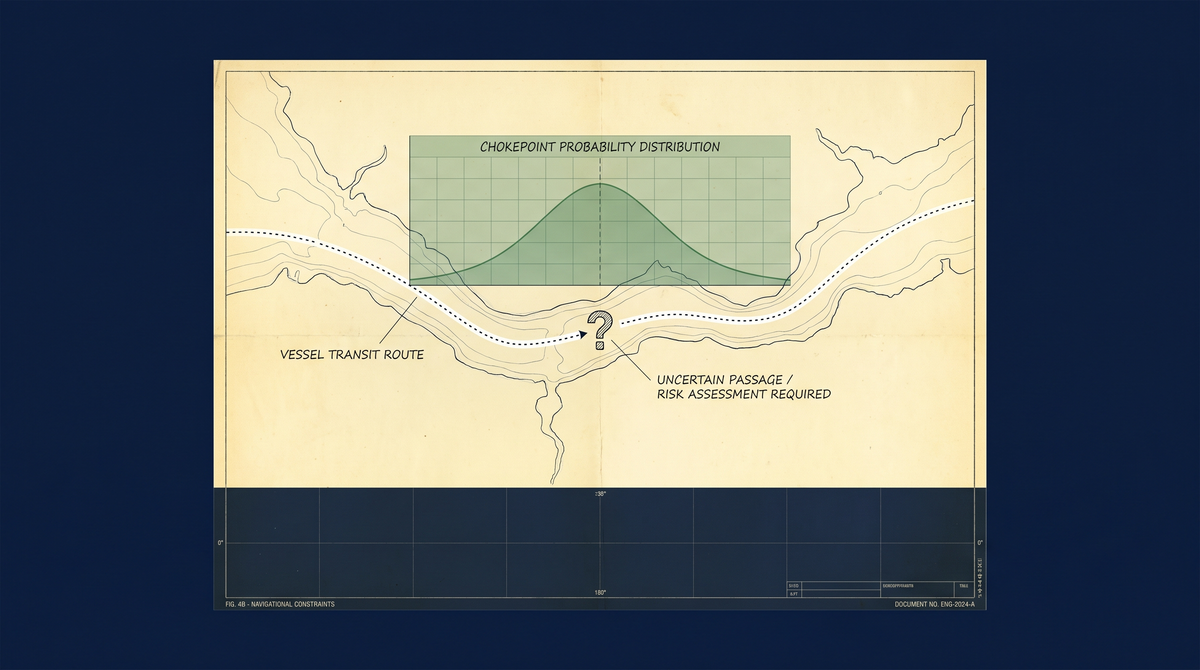

The probability distribution has shifted. "Messy prolonged situation with diplomatic resolution eventually" has become "messy prolonged situation with resolution path now genuinely unclear."

That distinction matters to energy markets not as an abstraction but as a pricing problem. The International Energy Agency warned last week that Europe has approximately six weeks of remaining jet fuel supply if the Strait does not normalize. European Union Commissioner Marta Kos confirmed this week that EU member states paid €22 billion more for fossil fuels in the first 45 days of the Middle East crisis alone. The EU's 27-member coordination effort is ongoing.

Six weeks is now inside the window. Every day without a clear diplomatic resolution is a day closer to that constraint becoming an operational problem rather than a forecast.

The ceasefire expiry and what it means

Trump told Bloomberg News the ceasefire will expire Wednesday night Eastern time and described extension as "highly unlikely." His public statements have oscillated between offering Iran "a very fair and reasonable deal" and threatening to "knock out every single Power Plant and every single Bridge in Iran."

That oscillation is itself an economic signal. Investors and companies making capital allocation decisions about AI infrastructure — which requires both cheap energy and access to debt markets priced on assumptions of geopolitical stability — cannot model this. The discount rate on long-horizon infrastructure investment does not require certainty about outcomes. It requires a credible range of possible outcomes. When the range includes resumed open hostilities in the world's most important oil transit chokepoint, the discount rate goes up. Quietly, before it shows up in any single data release.

At least 3,375 people have been killed in Iran since U.S. and Israeli attacks began approximately seven weeks ago, according to Iranian officials. The war is not a simulation.

What we are watching

The ceasefire expiry is Wednesday night. Before then, there are three possible outcomes: a deal is reached in Islamabad (unlikely based on current signals), the ceasefire is extended (Trump says no), or hostilities resume.

There is also a fourth possibility that the coverage has largely not addressed: that Iran attends talks and talks fail again, leaving the ceasefire in a legal gray zone — expired in name but not replaced by open conflict, with the U.S. naval blockade continuing indefinitely as the de facto state. That is arguably the worst outcome for energy markets: not a clean resolution in either direction, but a permanent ambiguity that keeps prices elevated without giving anyone a narrative on which to price stability.

The energy shock that was supposed to ease when the ceasefire was announced on April 7 has not eased. The mechanism — infrastructure damage, rerouted shipping, permanent alterations to supply chain geography — is exactly what The Ceasefire Asterisk predicted. The seizure of the Touska on Sunday is the confirmation.

Sources

- NPR: "Peace talks are in doubt as the U.S. seizes an Iranian ship" (April 20, 2026) — https://www.npr.org/2026/04/20/nx-s1-5791256/iran-middle-east-updates

- U.S. Central Command statement and video, April 20, 2026 — https://x.com/CENTCOM/status/2046085543348293851

- Iran's IRNA state news agency, via NPR, April 21, 2026

- President Trump Truth Social posts, April 20, 2026 — https://truthsocial.com/@realDonaldTrump/116433000897070863

- NPR / IMF World Economic Outlook: "Amid wars and soaring energy prices, IMF says the global economy is on the brink of recession" (April 18, 2026) — https://www.npr.org/2026/04/18/nx-s1-5786835/amid-wars-and-soaring-energy-prices-imf-says-the-global-economy-is-on-the-brink-of-recession

- IEA executive director warning, as cited in NPR/IMF WEO coverage

- Bloomberg News: Trump on ceasefire expiry and extension, via NPR

- New York Post, April 20, 2026 — https://nypost.com/2026/04/20/us-news/jd-vance-us-delegation-to-land-in-islamabad-within-hours-astrump-tells-the-post-nobodys-playing-games/