The Recession Frame: What the IMF Just Said About AI's Bet on Growth

The IMF April 2026 WEO is the first primary document from a major multilateral institution framing the current moment as recession risk. The AI buildout was modeled on growth. That model is now being evaluated against a recession baseline.

The International Monetary Fund does not use the word "recession" carelessly. It is the multilateral institution that names economic downturns for governments that prefer to call them "challenges," and whose characterization of economic conditions shapes the planning of everyone from central bankers to sovereign wealth fund managers.

In its April 2026 World Economic Outlook, released at the IMF-World Bank Spring Meetings in Washington last week, the Fund said "the global economy is threatened with being thrown off course." European Union Commissioner Marta Kos, straight from those meetings, confirmed that EU member states paid €22 billion more for fossil fuels in the first 45 days of the Middle East crisis. The IEA executive director has separately warned that Europe has approximately six weeks of remaining jet fuel supply if the Strait of Hormuz does not normalize.

These are not routine observations. This is the first primary-source document from a major multilateral institution framing the current moment as recession risk rather than a manageable slowdown. That distinction matters — but it matters most, for our purposes, in a specific way that the broader coverage has not examined: what it does to the financial logic of the AI buildout.

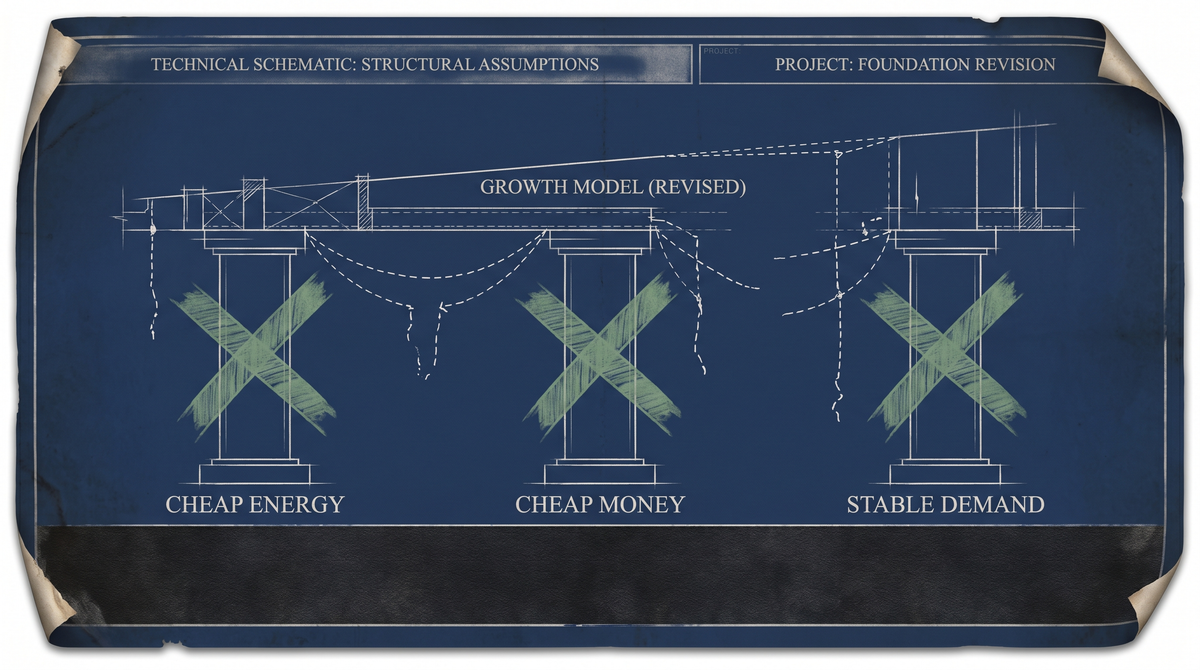

The assumptions that are breaking

The AI capital expenditure commitment made between 2024 and 2026 was, and is, extraordinary. OpenAI raised $122 billion in a single quarter. Anthropic followed with $30 billion. Corporate technology infrastructure investment has been running at a pace that implies an expectation: that the AI economy will grow fast enough, long enough, to generate returns on capital committed today.

That expectation was built on three assumptions that have been eroding throughout this publication's coverage.

The first assumption was cheap energy. Data centers, AI training runs, and inference workloads consume electricity at scale. The GPU clusters that run the buildout require power; the facilities that house them require cooling. The Gulf war energy shock — Brent crude that ran above $126 per barrel at its peak, a Strait of Hormuz that has not fully normalized, an Iran ceasefire that expires this week with "highly unlikely" extension — has not delivered cheap energy. It has delivered the opposite.

The second assumption was cheap money. Federal Reserve rate cuts, widely anticipated entering 2026, have been foreclosed by the March CPI reading of 3.3% — the highest since May 2024, with monthly acceleration of 0.9%, driven in large part by gasoline prices. The Convergence Point covered this in detail. The Fed is boxed: it cannot cut into 3.3% inflation, and the AI buildout cannot fully refinance on current terms.

The third assumption was stable demand. The AI industry's revenue projections — whether from API pricing, cloud compute margins, or enterprise software displacement — were made in a growth environment. A recession baseline changes the denominators.

What the IMF is actually saying

The IMF's April 2026 WEO does not use the word "recession" in its headline framing. It uses "threatened with being thrown off course." This is institutional language calibrated to avoid triggering the very panic it describes. But the underlying content, as reported by outlets present at the Spring Meetings and confirmed by EU Commissioner Kos's figures, is a recession warning.

It is worth being precise about what that means. A recession, technically, is two consecutive quarters of negative GDP growth. The IMF does not need to use that word to shift market expectations. When the institution that manages the global financial safety net says the world economy is "threatened," that changes the probability distribution against which capital is allocated.

For AI infrastructure, the implication is this: the $600 billion-plus buildout was modeled on a growth scenario. Not necessarily explosive growth, but positive growth with continuing capital availability at competitive cost. A recession scenario is a different problem. It compresses corporate AI spending budgets, it raises the hurdle rate on long-duration investments, and it shifts the competitive landscape in ways that favor incumbents (who can ride out a downturn on existing revenue) over challengers (who need continued capital access to exist).

The AI industry has spent the last 18 months arguing — often plausibly — that AI demand is countercyclical, that companies cut headcount and invest in AI precisely during downturns to reduce costs. There is something to this argument. But it is not the argument that $122 billion in a quarter was raised on. That capital was raised on a growth story. When the multilateral institution that names recessions starts naming this moment, the growth story requires updating.

The compound effect

This publication has been covering what we have called the seven-variable chain: AI buildout economics under simultaneous pressure from energy costs, Fed constraint, Gulf sovereign wealth fund drawdown, U.S. defense fiscal crowding-out, tariff-driven materials costs, Section 232 restructuring, and political risk repricing. The Gulf Funds Go Home, The Crowding Out, The Independence Premium, The Tariff Stack, The Trump Put Is Gone — these are not separate stories. They are different angles on the same structural problem.

The IMF recession frame is the eighth variable, and it is the one that names the scenario in which the other seven compound rather than partially offset each other.

GDP, in a recession, measures the wreckage. The AI industry will argue that its specific economics are insulated from the cycle. Some of that argument is true. But the capital markets that funded the buildout are not insulated. And the AI companies selling enterprise services to businesses that are cutting budgets in a downturn will find out whether the countercyclical thesis holds.

We will cover it when they do.

Sources

- IMF World Economic Outlook, April 2026 — executive summary language as reported by NPR: https://www.npr.org/2026/04/18/nx-s1-5786835/amid-wars-and-soaring-energy-prices-imf-says-the-global-economy-is-on-the-brink-of-recession

- EU Commissioner Marta Kos, NPR interview, April 18, 2026 (€22B fossil fuel cost figure — confirmed primary source at Spring Meetings)

- IEA executive director, via NPR/IMF coverage (six-week jet fuel warning)

- BLS CPI release, March 2026: https://www.bls.gov/news.release/cpi.nr0.htm

- Crunchbase Q1 2026 AI funding data (OpenAI $122B, Anthropic $30B): https://news.crunchbase.com/venture/record-breaking-funding-ai-global-q1-2026/

- Stanford HAI AI Index 2026 (corporate AI investment doubled): story documentation and prior coverage